How Much Does Life Insurance Cost in Australia? (2026)

Life insurance in Australia typically costs between $17 and $300+ per month, depending on your age, cover amount, smoking status and how you buy.

See your real cost instantly - no contact details required.

Get your personalised estimate

How Much Does Life Insurance Cost in Australia?

Life insurance in Australia costs between $17 and $300+ per month. Most Australians pay between $25 and $150 per month, with the exact amount depending on age, cover level, smoking status and the insurer you choose.

To give you a concrete starting point, here are example monthly premiums from leading insurers for a 25-year-old male non-smoker with $500,000 cover:

- Zurich - from $17/month

- OnePath - from $18/month

- Acenda - from $23/month

- Encompass - from $23/month

- Neos - from $26/month

Based on $500,000 cover, clerical occupation, stepped premiums.

Average Life Insurance Premiums by Age, Gender and Smoking Status

Age is the single biggest driver of life insurance cost. Premiums roughly double between your 30s and 50s, and smokers typically pay up to twice as much as non-smokers at the same age.

| Age Band | Male Non-Smoker | Male Smoker | Female Non-Smoker | Female Smoker |

|---|---|---|---|---|

| 25-29 | $26 | $46 | $18 | $35 |

| 30-34 | $22 | $43 | $17 | $33 |

| 35-39 | $21 | $48 | $17 | $35 |

| 40-44 | $24 | $64 | $19 | $45 |

| 45-49 | $36 | $102 | $29 | $68 |

| 50-54 | $67 | $176 | $52 | $113 |

| 55-59 | $205 | $322 | $103 | $205 |

Example pricing: $500,000 cover, clerical occupation, stepped premiums. Based on real insurer pricing across multiple Australian providers.

What Affects the Cost of Life Insurance?

Seven factors determine how much you pay. Age and smoking status have the biggest impact - but insurer choice is often overlooked and can make a significant difference.

| Factor | Impact on your premium |

|---|---|

| Age | Premiums increase significantly from age 45 onwards |

| Smoking | Adds 30-100% depending on product and age |

| Gender | Males pay more for life cover; females pay more for income protection |

| Premium type | Variable vs Age-Stepped changes your long-term total cost significantly |

| Health history | Insurers can apply premium loadings or exclusions based on your health and medical history |

| Insurer | Almost identical cover from different insurers can vary by over 50% in price |

| How you buy | Some advisers will charge a fee as well as commisson. Some companies can give effective discounts of 10% or more as cashbacks or rebates - it's worth shopping around. |

Why Comparing Providers Can Save You 50% or More

Life insurance prices vary significantly between insurers. For the same person and the same cover, premiums can differ by 50% or more. A recent review found one insurer pricing a TPD policy at age 55 at 96% more than a competitor offering equivalent cover.

Beyond the base price, how you buy matters too. Some advisers charge fees on top of commissions. Some channels - including Keep Insurance - return part of the commission back to you as a cashback of up to 12.5% of your premium every year. Over a 10- or 20-year policy, that adds up materially.

Compare Life Insurance QuotesSee real prices from leading insurers in minutes

How You Buy Life Insurance Affects the Price

The channel you use to buy life insurance can be as important as the insurer you choose. Here's how the main options compare:

Through super

Often one of the cheaper ways to get basic cover, but cover levels and flexibility are limited compared to retail policies. Not always the best value for meaningful cover amounts.

Direct (over the phone)

Convenient but typically more expensive. Research shows direct policies can cost 50% more - and in some cases up to 4× more than equivalent retail cover.

Is direct insurance worth the cost?Financial adviser

Personal advice adds value for complex situations, but can include advice fees on top of commissions - increasing the effective cost of your cover.

Insurance broker

Brokers can compare products and pricing, but don't provide personal advice. Some may have limited insurer panels or retain full commissions.

Tip: Look for brokers that offer rebates or cashback options.

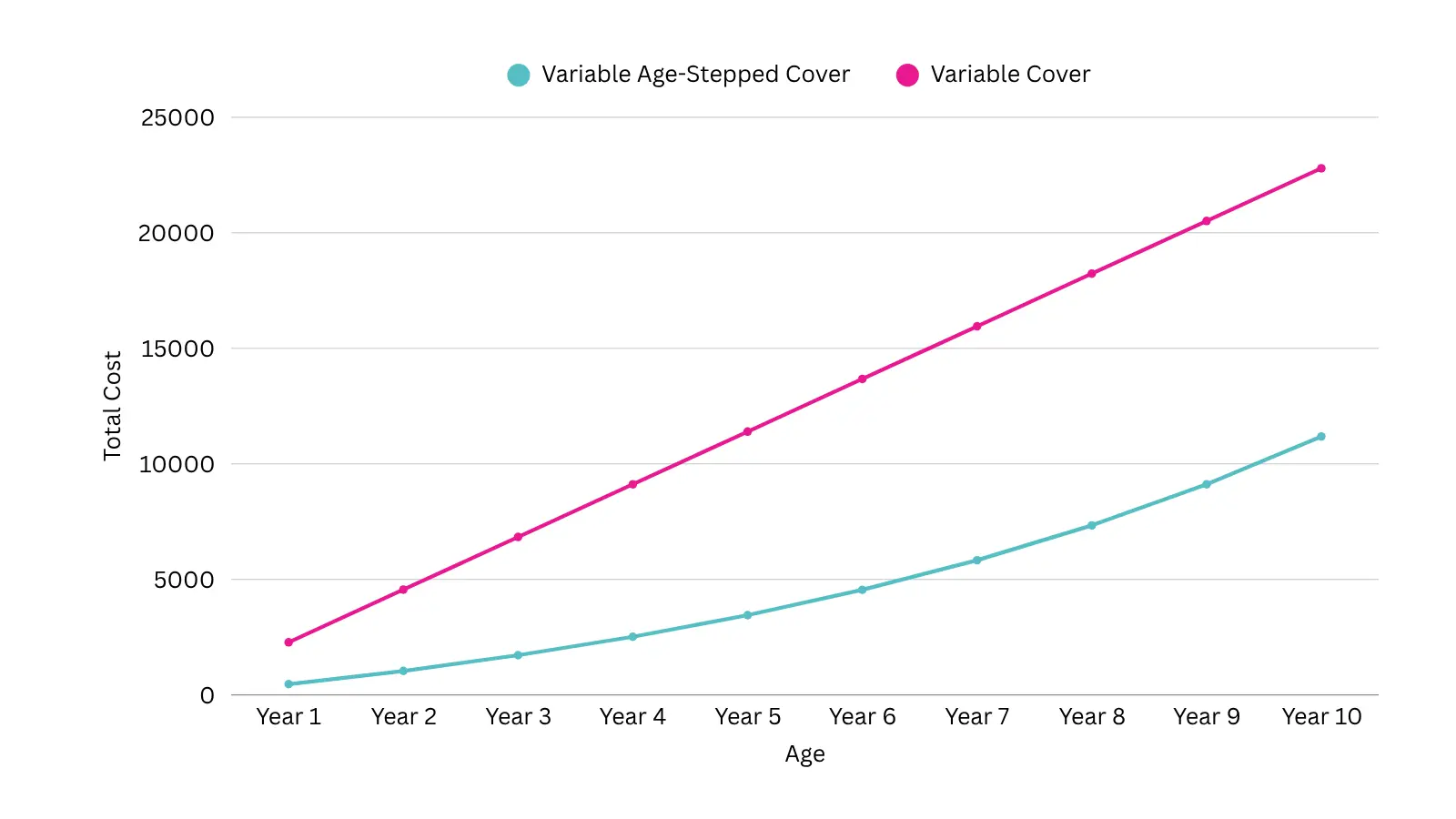

Stepped vs Level Premiums - Which Costs Less Long Term?

Stepped premiums are cheaper initially but increase each year as you age. Level premiums start higher but are usually cheaper overall if you hold the policy for more than 10 years.

How Smoking Affects Life Insurance Costs

Smoking is one of the most significant premium factors insurers apply. On average, smokers pay:

- ›Up to 100% more for life insurance

- ›30-50% more for income protection

The exact loading depends on your age, cover amount and insurer.

If you have been smoke-free for 12 months, many insurers will reclassify you as a non-smoker - which can significantly reduce your premiums. It's worth requesting a reassessment once you reach this milestone.

How to Reduce Your Life Insurance Premiums

If your premiums feel high, there are several ways to reduce what you pay - often without reducing your cover:

- Compare insurers - prices for the same cover can vary by 50% or more between providers

- Adjust your cover amount to better reflect your actual financial obligations

- Switch premium structure - moving from stepped to level can reduce long-term total cost if you're holding cover past 10 years

- Quit smoking - after 12 months smoke-free, request reclassification from your insurer

- Use a cashback or rebate structure - some brokers return part of their commission to you, reducing your effective annual cost without changing the policy

Life insurance is just one part of protecting your income and family. If you're comparing costs for cover that replaces your salary if you can't work, see our guide to income protection costs in Australia.

Frequently Asked Questions

How much does life insurance cost in Australia? +

Life insurance in Australia typically costs between $17 and $300+ per month, depending on your age, cover amount, smoking status and the insurer you choose. Most Australians pay between $25 and $150 per month.

How much does $500,000 of life insurance cost per month? +

For a non-smoker, $500,000 of cover typically costs $17-$30 per month in your 20s, $20-$40 per month in your 30s, and $50-$210 per month in your 50s. Costs increase with age, and smokers pay significantly more.

How much does $1 million of life insurance cost per month? +

For a non-smoker, $1 million of cover typically costs $35-$80 per month in your 20s and $200-$450+ per month in your 50s, depending on your age, health and smoking status.

What factors affect life insurance costs in Australia? +

The main factors are age, smoking status, gender, health history, occupation, the amount of cover, and the premium structure (stepped vs level). The insurer and how you buy can also make a significant difference to what you pay.

Why do premiums increase with age? +

As you age, the statistical risk of illness and death increases. Insurers adjust premiums to reflect this, especially on stepped policies which increase every year at renewal.

Do all insurers charge the same for life insurance? +

No. Premiums for the same cover can vary by 50% or more between insurers, depending on their pricing models, underwriting approach and policy structure. Comparing quotes is one of the most effective ways to reduce what you pay.

Is life insurance expensive in Australia? +

Life insurance can be affordable when you're younger, with policies starting from around $17-$20 per month. Costs increase significantly with age and risk factors. Comparing insurers and choosing the right premium structure can help manage costs over time.

Show more questions

Is stepped or level life insurance cheaper? +

Stepped premiums are cheaper initially but increase each year as you age. Level premiums start higher but can be more cost-effective overall if you hold the policy for more than 10 years.

Why do smokers pay more for life insurance? +

Smoking significantly increases the risk of serious illness and death, which leads insurers to charge higher premiums - often up to double compared to non-smokers of the same age.

Can I be reclassified as a non-smoker? +

Yes. After 12 consecutive months without smoking, many insurers will reclassify you as a non-smoker, which can significantly reduce your premiums. Contact your insurer or broker to request a reassessment.

Can I reduce my life insurance premiums without changing my cover? +

In some cases, yes. Comparing insurers, switching premium structures, or using a broker who returns part of their commission as cashback can all reduce your effective annual cost without changing the underlying cover.

Can I get money back from life insurance premiums? +

Some brokers and advisers return part of their commission to you as a cashback or rebate - reducing the real cost of your cover over time. Keep Insurance offers up to 12.5% of your premium back every year on eligible policies.

Key Takeaways: Life Insurance Costs in Australia (2026)

- Most Australians pay between $25 and $150 per month for life insurance

- Premiums increase significantly from age 45 onwards

- Smokers pay up to double the premium of non-smokers

- Prices for identical cover can vary by 50% or more between insurers

- Stepped premiums are cheaper initially; level premiums are often better value long term

- Some buying channels offer cashback or rebates that reduce your effective annual cost